BRISBANE SOUTHSIDE LEASING

The Industrial leasing market continues to perform strongly in the Brisbane Southside Industrial precincts. An analysis of leasing data by specialist industrial property consultants King & Co of established industrial buildings shows that the industrial leasing team has leased, on average, 195,230 square metres of industrial accommodation over the last three financial years to end of May 2018.

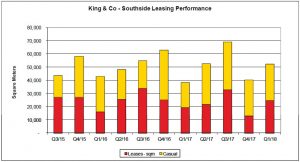

The data shows that FY 2017 was the strongest year with 208,662 square metres of accommodation leased at an average rental of $101.29 for leases with a term of 6 months or more. Average industrial rentals for established stock grew by 6.24% over the corresponding period in 2016. This was a strong result as the volume of leasing transactions actually fell for the same period from 121 to 92 transactions. This pointed to a reduction in available stock in the market as well as increased demand for industrial accommodation.

The FY 2018 data showed a continuation of that strong performance, with Quarter 3 2017 posting a very solid 32,695 square metres, which was second only to Quarter 3 2016, with 33,806 square metres. As at May 2018 the market has not surged above the FY2017 level, but FY 2018 is still forecast to post another very solid year with 79,223 square metres of accommodation leased to the end of May 2018. With a monthly leasing average of over 8,200 square metres, FY 2018 is still forecast to exceed 87,000 square metres.

The graph below tracks King & Co’s Brisbane Southside Industrial Leasing performance on a quarterly basis for the last three financial years. The data is split into leases of 6 months or more duration and casual leases.

Other market indicators also pointed to a solidly performing market. Average rentals have maintained the gains made in FY17. Average rentals for the FY 2016 showed $95.35 per square metre, rising to $101.29 in FY17, a 6.24% increase. The year to May 18 shows an average rental of $99.13 per square metre, which indicates that demand remains strong and stock supply is falling.

The average lease term rose from 2.46 years in FY16 to 2.73 years in FY17, an increase of 10.79%. This corresponds with the level of activity seen in that period. As at May 2018, the average lease term has remained steady at 2.6 years. Typically established buildings are generally older stock which struggles to get good lease tenure, however the three year analysis shows that demand has remained consistent for the 2018 financial year. The analysis excludes monthly and casual leasing arrangements which are a feature of some older buildings in the established southside suburbs.

The monthly and casual leasing market has followed similar trends. The amount of accommodation leased rose from to 96,959 square metres in FY16 to 108,628 in FY17. As at May 18, there was 104,770 square metres of this accommodation leased. The average rent for monthly and casual leasing is showing a slight increase in FY18, with an average rate of $50.22 showing a modest 1.5% gain on the previous year.

The analysis shows that the monthly and casual leasing market, as a proportion of the total market is growing, with a compound growth rate of 4.7% over the period of the analysis. This accommodation is almost exclusively within secondary buildings and the numbers are not truly reliable as each monthly lease is recorded. Therefore a casual tenant, who stays for 3 months, will have that accommodation recorded three times. So whilst landlords of secondary stock need to remain flexible to meet the needs of the market, the data does not suggest a long term trend away from more permanent tenancy arrangements.

In an attempt to get a more realistic indicator of market activity in the southside industrial leasing market, the King & Co analysis deliberately removes design and construction activity. The Design and construct market is a legitimate market in its own right, but is dominated by institutional owners and corporate style tenants and is considered less transparent than the leasing market for existing stock. Economic and financial factors such as land cost, construction costs, tenant specific requirements and lease incentives all play a role in influencing the design and construct market, whereas the established leasing market is a broader and more genuine indicator of economic activity in the southside industrial employment hubs. This is an attempt to get a real guage on the pulse of the southside industrial lease market.

This trend of increasing demand should see rents continue to rise and length of tenure increase into the medium term.

Peter Roberts

Director Professional Services

& Property Management

m: 0412 055 884

June 2018